02/26/2012

Spain - Iberdrola's renewable energy capacity grows by 1.1GW in 2011 to reach 13.69 GW

Despite difficult economic environment and €402 million in writedowns. Ebitda rose 1.6% to €7.65 billion helped by a balanced and diversified business portfolio and grounded in efficiency measures, international spread and solid finances. Sales rose 4% to €31,648 million and operating cash flow rose 5.8% to €6,047 million. The tax burden for liberalized businesses rose 50% to €621 million, of which €518 million corresponded to Spain where this ítem has more than doubled in two years. Operating efficiency improved 1.7% in the year. Investments came to more than €8.1 billion during the year, in existing businesses and on international expansion. A proposal will be submitted to the General Shareholders Meeting to maintain 2011 dividend at a gross €0.326/share.

Iberdrola, having raised €8.91 billion in financing last year, has liquidity of €9.3 billion, enough to cover requirements for the next 24 months. The Company’s balance sheet strength, with equity totalling €33,208 million, has enabled it to maintain its “A” credit ratings with a stable outlook. The Company maintains its projection for Ebitda growth at around 5% for the period 2010-2012.

Iberdrola’s net profit for 2011 came to €2,805 million, a small decline of 2.3% over 2010, while Ebitda hit the highest level in its history at €7,650.5 million, a rise of 1.6%. This was achieved despite Group writedowns, difficult economic circumstances, and lower extraordinary income.

Writedowns came to a gross €402 million and reflect three principal factors: revised capacity use estimations at the Longannet coal-fired plant in the UK, new projections relating to Gamesa’s business plan and the development cost of renewables projects that have been abandoned.

Added to this have been a challenging economic environment, with falling demand and lower prices, as well as regulatory changes for renewables, a sharp increase in taxation and currency factors. An additional factor has been a €133 million fall in extraordinary income, reflecting the sale in 2010 of assets in Guatemala and Connecticut.

Ebitda was nevertheless underpinned by solid performance in the regulated and renewables businesses, which contributed 51% and 19% respectively to the Group total. Regulated business Ebitda rose 5.5% to €3,825.4 million and renewables held stable at €1,455.6 million.

Performance in these two areas – regulated business and renewables – offset the results in liberalised businesses which although they contributed 30% to Group Ebitda registered a 7.4% drop to €2,255.1 million in this item. This was mainly due to a sharp increase in taxes which last year rose 50.1% to €621 million including €518 million corresponding to Spain.

The Company carried out investments totalling €8.19 billion, of which €4,002 million was in existing businesses with 44% in the regulated area, 39% in renewables, 12% in liberalized business and 5% in other areas. It also invested €1,672 million last April to acquire Elektro in Brazil, and disbursed €2,516 million for the merger by absorption with Iberdrola Renovables.

Cash flow was 5.8% higher at €6,047 million, while revenues rose 4% to €31,648 million and gross margin rose 3.3% to €12,026 million, sustained by a diversified business model and international reach. Efficiency improved 1.7% over the previous year. Production was 5.5% lower at 145,126 gigawatt hours (GWh), reflecting a 19.6% drop in cogeneration and 18% in hydroelectric output. Renewable production nonetheless continued to improve, rising 13.1% to 28,721 GWh.

On the strength of these results, the Company maintains its projections for Ebitda growth at 5% for the period 2010-2012.

Solid finances and “A” rating consolidated:

Despite the tough economic environment, IBERDROLA continued to strengthen its finances in 2011, with liquidity at close to €9.3 billion, enough to cover needs for 24 months. Equity stood at €33,208 million.

Group net adjusted debt - excluding the €2,991 million pending from the tariff deficit – came to €28,715 million at the end of 2011, an increase of 15.9% over 2010 due to the share buyback relating to the merger by absorption with Iberdrola Renovables and to the acquisition of Elektro.

The Group nonetheless succeeded in maintaining leverage at 46.4% (excluding the deficit), while the financial result improved 17.5% to €1,061.9 million.

IBERDROLA raised €8.91 billion in financing during the year, as a result of which the average life of its debt stood at 6.3 years, with 80% of debt maturing in 2012 already refinanced. This enabled the Company to maintain its “A” ratings with a stable outlook, at a time of widespread downgrades.

Shareholder remuneration policy maintained:

IBERDROLA maintained its shareholder remuneration policy throughout 2011, launching two new instalments of its Iberdrola Flexible Dividend both for the final 2010 dividend and also for the 2011 interim payment. This plan offers shareholders the option of receiving their dividends through tax-free shares, or to sell the rights to the Company – at a guaranteed fixed price – or to the market.

The Board of Directors of IBERDROLA, on Monday resolved to submit to the General Shareholders Meeting a proposal for a 2011 dividend payment amounting to at least the €0.326 gross payment per share paid last year.

To this end, IBERDROLA will in the first instance propose a cash dividend of €0.03 gross per share and a new instalment of the Iberdrola Flexible Dividend scrip dividend plan. Under this plan, the Company commits to acquiring the rights for at least €0.15 before tax.

This gross payment of €0.18 per share would be in addition to the €0.146 purchase price for rights under the Iberdrola Flexible Dividend paid out in January – corresponding to the interim 2011 dividend – to reach the total of €0.326 gross payment per share.

Key operating data in 2011:

1) Growth in regulated businesses

Ebitda for regulated businesses rose 5.5% to €3,825.4 million, reflecting progress in various regulatory aspects as well as synergies and best practices across the Group. By geographical area, Spain contributed €1,555.4 million (40.65% of the total), Brazil €890.2 million (23.27%), the UK €832.3 million (21.75%) and the United States €547.7 million (14.31%).

Performance in Brazil stands out, providing the second largest country contribution to Ebitda with a rise of 59.9% resulting from consolidation of Elektro, the appreciation of the real currency and new hydroelectric capacity on stream. Excluding Elektro, Ebitda from Brazil would have risen 3.8%.In the UK, regulated business Ebitda rose 4.2% as a result of a 5% rise in revenues generated by investments which rose 10% and increased efficiency.

2) Liberalized business affected by higher taxation

Ebitda from liberalized businesses fell 7.4% to €2,255 million, due mainly to a 50.1% rise in taxation. In Spain, it rose 5.9% to €1,570.7 million as a result of higher margins despite the fact tax payments increased 30.5%. In just two years, the tax burden in Spain has almost doubled to €517.6 million last year, corresponding to the social bonus, nuclear taxes and efficiency measures.

In the UK, Ebitda fell 40.8% to €322.5 million due to lower output and sales of electricity and gas, as well as tighter electricity margins. This performance should improve in 2012. Liberalized business in Mexico also declined by 11.1% to €361.9 million, mainly due to the impact of asset sales in Guatemala in 2011 and currency factors.

3) Renewables maintain ebitda levels

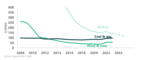

Ebitda from renewables business came to €1,455.6 million, similar to the previous figure. Installed capacity rose 9.2% to 13,690 megawatts (MW) across the Group, with 579 MW currently in construction.

Of the more than 1,100 MW installed in 2011, more than 84% was outside Spain, reflecting the strategy of diversification. Of total installed capacity, 57% is outside Spain. In addition to its leadership in onshore wind farm, Iberdrola also leads in offshore wind power development with more than 5,500 MW under development in the UK and Germany.

It is also pioneering development marine energy technologies. Last year it installed a Pelamis prototype wave energy device off the coast of Orkney, and continued developing the 1 MW Hammerfest Strom pilot for tidal energy. In this context, the Sound of Island project, which envisages 10 MW of tidal capacity, continues on schedule.

For more information on this article or if you would like to know more about what www.windfair.net can offer, please do not hesitate to contact Trevor Sievert at ts@windfair.net

www.windfair.net is the largest international B2B Internet platform – ultimately designed for connecting wind energy enthusiasts and companies across the globe!

Iberdrola, having raised €8.91 billion in financing last year, has liquidity of €9.3 billion, enough to cover requirements for the next 24 months. The Company’s balance sheet strength, with equity totalling €33,208 million, has enabled it to maintain its “A” credit ratings with a stable outlook. The Company maintains its projection for Ebitda growth at around 5% for the period 2010-2012.

Iberdrola’s net profit for 2011 came to €2,805 million, a small decline of 2.3% over 2010, while Ebitda hit the highest level in its history at €7,650.5 million, a rise of 1.6%. This was achieved despite Group writedowns, difficult economic circumstances, and lower extraordinary income.

Writedowns came to a gross €402 million and reflect three principal factors: revised capacity use estimations at the Longannet coal-fired plant in the UK, new projections relating to Gamesa’s business plan and the development cost of renewables projects that have been abandoned.

Added to this have been a challenging economic environment, with falling demand and lower prices, as well as regulatory changes for renewables, a sharp increase in taxation and currency factors. An additional factor has been a €133 million fall in extraordinary income, reflecting the sale in 2010 of assets in Guatemala and Connecticut.

Ebitda was nevertheless underpinned by solid performance in the regulated and renewables businesses, which contributed 51% and 19% respectively to the Group total. Regulated business Ebitda rose 5.5% to €3,825.4 million and renewables held stable at €1,455.6 million.

Performance in these two areas – regulated business and renewables – offset the results in liberalised businesses which although they contributed 30% to Group Ebitda registered a 7.4% drop to €2,255.1 million in this item. This was mainly due to a sharp increase in taxes which last year rose 50.1% to €621 million including €518 million corresponding to Spain.

The Company carried out investments totalling €8.19 billion, of which €4,002 million was in existing businesses with 44% in the regulated area, 39% in renewables, 12% in liberalized business and 5% in other areas. It also invested €1,672 million last April to acquire Elektro in Brazil, and disbursed €2,516 million for the merger by absorption with Iberdrola Renovables.

Cash flow was 5.8% higher at €6,047 million, while revenues rose 4% to €31,648 million and gross margin rose 3.3% to €12,026 million, sustained by a diversified business model and international reach. Efficiency improved 1.7% over the previous year. Production was 5.5% lower at 145,126 gigawatt hours (GWh), reflecting a 19.6% drop in cogeneration and 18% in hydroelectric output. Renewable production nonetheless continued to improve, rising 13.1% to 28,721 GWh.

On the strength of these results, the Company maintains its projections for Ebitda growth at 5% for the period 2010-2012.

Solid finances and “A” rating consolidated:

Despite the tough economic environment, IBERDROLA continued to strengthen its finances in 2011, with liquidity at close to €9.3 billion, enough to cover needs for 24 months. Equity stood at €33,208 million.

Group net adjusted debt - excluding the €2,991 million pending from the tariff deficit – came to €28,715 million at the end of 2011, an increase of 15.9% over 2010 due to the share buyback relating to the merger by absorption with Iberdrola Renovables and to the acquisition of Elektro.

The Group nonetheless succeeded in maintaining leverage at 46.4% (excluding the deficit), while the financial result improved 17.5% to €1,061.9 million.

IBERDROLA raised €8.91 billion in financing during the year, as a result of which the average life of its debt stood at 6.3 years, with 80% of debt maturing in 2012 already refinanced. This enabled the Company to maintain its “A” ratings with a stable outlook, at a time of widespread downgrades.

Shareholder remuneration policy maintained:

IBERDROLA maintained its shareholder remuneration policy throughout 2011, launching two new instalments of its Iberdrola Flexible Dividend both for the final 2010 dividend and also for the 2011 interim payment. This plan offers shareholders the option of receiving their dividends through tax-free shares, or to sell the rights to the Company – at a guaranteed fixed price – or to the market.

The Board of Directors of IBERDROLA, on Monday resolved to submit to the General Shareholders Meeting a proposal for a 2011 dividend payment amounting to at least the €0.326 gross payment per share paid last year.

To this end, IBERDROLA will in the first instance propose a cash dividend of €0.03 gross per share and a new instalment of the Iberdrola Flexible Dividend scrip dividend plan. Under this plan, the Company commits to acquiring the rights for at least €0.15 before tax.

This gross payment of €0.18 per share would be in addition to the €0.146 purchase price for rights under the Iberdrola Flexible Dividend paid out in January – corresponding to the interim 2011 dividend – to reach the total of €0.326 gross payment per share.

Key operating data in 2011:

1) Growth in regulated businesses

Ebitda for regulated businesses rose 5.5% to €3,825.4 million, reflecting progress in various regulatory aspects as well as synergies and best practices across the Group. By geographical area, Spain contributed €1,555.4 million (40.65% of the total), Brazil €890.2 million (23.27%), the UK €832.3 million (21.75%) and the United States €547.7 million (14.31%).

Performance in Brazil stands out, providing the second largest country contribution to Ebitda with a rise of 59.9% resulting from consolidation of Elektro, the appreciation of the real currency and new hydroelectric capacity on stream. Excluding Elektro, Ebitda from Brazil would have risen 3.8%.In the UK, regulated business Ebitda rose 4.2% as a result of a 5% rise in revenues generated by investments which rose 10% and increased efficiency.

2) Liberalized business affected by higher taxation

Ebitda from liberalized businesses fell 7.4% to €2,255 million, due mainly to a 50.1% rise in taxation. In Spain, it rose 5.9% to €1,570.7 million as a result of higher margins despite the fact tax payments increased 30.5%. In just two years, the tax burden in Spain has almost doubled to €517.6 million last year, corresponding to the social bonus, nuclear taxes and efficiency measures.

In the UK, Ebitda fell 40.8% to €322.5 million due to lower output and sales of electricity and gas, as well as tighter electricity margins. This performance should improve in 2012. Liberalized business in Mexico also declined by 11.1% to €361.9 million, mainly due to the impact of asset sales in Guatemala in 2011 and currency factors.

3) Renewables maintain ebitda levels

Ebitda from renewables business came to €1,455.6 million, similar to the previous figure. Installed capacity rose 9.2% to 13,690 megawatts (MW) across the Group, with 579 MW currently in construction.

Of the more than 1,100 MW installed in 2011, more than 84% was outside Spain, reflecting the strategy of diversification. Of total installed capacity, 57% is outside Spain. In addition to its leadership in onshore wind farm, Iberdrola also leads in offshore wind power development with more than 5,500 MW under development in the UK and Germany.

It is also pioneering development marine energy technologies. Last year it installed a Pelamis prototype wave energy device off the coast of Orkney, and continued developing the 1 MW Hammerfest Strom pilot for tidal energy. In this context, the Sound of Island project, which envisages 10 MW of tidal capacity, continues on schedule.

For more information on this article or if you would like to know more about what www.windfair.net can offer, please do not hesitate to contact Trevor Sievert at ts@windfair.net

www.windfair.net is the largest international B2B Internet platform – ultimately designed for connecting wind energy enthusiasts and companies across the globe!

- Source:

- IBERDROLA

- Author:

- Posted by Trevor Sievert, Online Editorial Journalist

- Email:

- ts@windfair.net

- Link:

- www.windfair.net/...

- Keywords:

- IBERDROLA; wind, wind energy, wind turbine, rotorblade, awea, ewea, wind power, suppliers, manufacturerstrevor sievert

- Wind Energy Wiki:

- Wave Energy